China’s Zijin Mining: China’s Push for Gold, Copper, and Control from Tibet to Ghana

Credit: Ainvest.com

China’s Zijin Mining Group has become a key instrument in Beijing’s drive to lock down strategic minerals from Tibet to Africa, tightening China’s grip over critical supply chains and vulnerable states. Behind record profits and ambitious 2026 output targets lies a geopolitical project that fuses resource extraction with power projection, entrenching Chinese influence while exporting environmental damage, governance risks, and sovereignty erosion to frontline regions from the Himalayan plateau to Ghana and Kazakhstan.

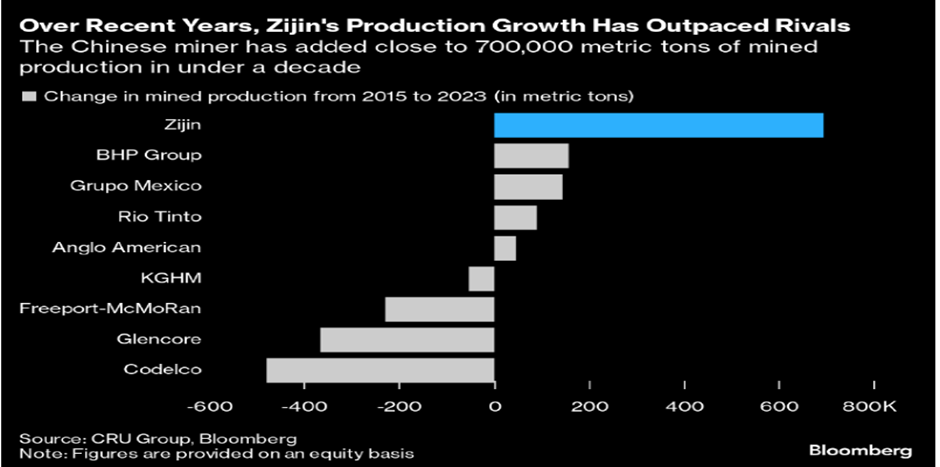

Zijin Mining reported estimated 2025 net income of about 52 billion yuan (around 7.4 billion dollars), driven by record prices for copper, gold, and silver. This profit surge gives Beijing-backed capital even greater leverage to acquire assets abroad and deepen its control over critical supply chains.

The company plans double-digit growth in 2026, targeting 105 tonnes of mined gold and 1.2 million tonnes of copper, representing 17% and 10% year‑on‑year increases respectively. Such expansion is not just a business story but a geopolitical project, aligning with China’s long-term strategy to dominate minerals that underpin military industries and green technologies.

Tibet: mining under occupation

A key driver of Zijin’s growth is the expansion of its Julong copper mine in China’s Tibet region, a territory whose political status and human rights situation are already deeply contested. Turning Tibet into an extraction frontier strengthens Beijing’s economic grip over the plateau while marginalising local voices and accelerating environmental degradation in a fragile, high-altitude ecosystem.

Copper mining at scale in Tibet risks contaminating water sources that feed major Asian rivers, affecting downstream communities far beyond China’s borders. By tying Tibet’s economy to state-linked mining conglomerates, Beijing further normalises occupation under the guise of “development” and “green transition” rhetoric.

Global acquisitions, local risks

Zijin’s march to a 100‑tonne annual gold output target now expected two years ahead of schedule is powered by a wave of acquisitions, including gold mines in Ghana and Kazakhstan. These deals extend Chinese state-linked influence deep into resource-rich regions where governance challenges and debt vulnerabilities already create fertile ground for strategic dependence.

The company’s pattern of buying high-quality assets across multiple continents has been praised by some market analysts, but for host countries it concentrates ownership in the hands of a foreign power with clear geopolitical ambitions. Communities in Africa, Central Asia, and Latin America have repeatedly raised concerns over labour practices, environmental standards, and the lack of transparent benefit-sharing in Chinese mining projects.

Zijin’s Hong Kong–listed shares more than doubled to a record high in 2025, with the stock trading around HK$36.50 at the end of the year. This stock market success translates into cheaper capital and greater firepower for further acquisitions, reinforcing a feedback loop in which financial gains fuel strategic expansion. Its recently spun-off unit, Zijin Gold International, projects 2025 net profit of roughly 1.5–1.6 billion dollars, a year‑on‑year surge of about 212%–233%. With such cash flows, Chinese mining champions can outbid competitors, lock up future production, and quietly rewrite the rules of global resource governance in Beijing’s favour.

China’s Zijin Mining Group aggressively expands in Tibet’s Julong copper mine, turning the fragile Himalayan plateau into a resource extraction zone under Beijing’s control. Large-scale mining accelerates ecological devastation: toxic tailings pollute sacred rivers like the Brahmaputra and Mekong, threatening downstream water security for millions in India, Bangladesh, and Southeast Asia. Glacier melt from mining emissions worsens climate vulnerability, while deforestation and habitat loss drive biodiversity collapse. This state-backed plunder normalises occupation, exports environmental harm, and undermines regional sovereignty for China’s mineral dominance.

Copper and gold are not neutral commodities; copper is essential for defence electronics, infrastructure, and the so‑called green transition, while gold remains a backbone of financial resilience and sanctions-proof reserves. By racing toward 1.2 million tonnes of copper output and rapidly scaling gold production, Zijin strengthens China’s hand in any future economic or geopolitical crisis where control of critical materials becomes a tool of coercion.

Far from being a simple corporate success story, Zijin Mining’s record profits and output push expose a hard reality: China is weaponizing state-backed resource giants to entrench dominance from Tibet to Africa, reshaping regional power balances while local communities carry the environmental and sovereignty costs.